Introduction/Background

There has been plenty of research and evidence showing that stock prices can be predicted and are affected by various aspects of daily life, which can ultimately help an investor. For example, the general news occurring in the world and country can affect the movement of certain stocks directly and indirectly. However, much of the research in this field is centered around financial news, rather than the news as a whole. With this in mind, our team is looking to analyze the immediate change of stock prices as a reaction to general news. To better understand the difference between a stable stock and a more volatile entity, we will be using both Apple stock and Bitcoin prices for this project.

Problem Definition

This machine learning project focuses on analyzing news stories to predict the movement of Bitcoin (BTC) and Apple (AAPL) stock prices in the market. Research has shown that “inclusion of predictors [like] news articles and twitter posts can significantly improve the quality of stock price predictions” (Vanstone et al., 2019). For this midpoint, we focused on AAPL, and will extend to BTC moving forward. We do not expect this extension to take very long, as it would just require using BTC data instead of APPL data in our existing model. Instead of looking at purely apple-related or financial news, our model will be looking at news as a whole. Also, we shifted from simply predicting the rise and fall of AAPL to predicting the exact daily change in stock price. We are looking to find a correlation between the stock prices of AAPL and BTC and general news stories in the coming weeks to aid in investment decisions for both people and companies.

Data Collection

We obtained our news article data from the NYT Developer API, taking the NYT archive data from January 2016 to

December 2020. By feeding the month and year to the API, we get JSON with an array of all articles from that

particular month. Rather than the full raw text of all the articles, we receive the metadata from these articles

such as headlines, abstract, and keywords. Thus, the NYT data was already relatively clean and extensive data

cleaning wasn’t needed. It was helpful to use the cleaned data rather than raw text from all the articles to avoid

storage and computing issues in our model. To obtain AAPL data, we used the yfinance library to access historical

financial AAPL stock data from Yahoo Finance from December 2015 to January 2021 (we added these two extra months to

account for price changes from January 2016 to December 2020). Though this data was also relatively clean, we still

had to perform some data cleaning and preprocessing before our data was ready. For example, we added extra features

to the Apple data that were not present in Yfinance like the percent change for a day. We also removed the news

article data from days the stock market was not open, including weekends and holidays, to ensure our model was using

the appropriate data.

The content of interest in the NYT news articles was the abstract. We decided to use BERT because “it’s conceptually

simple” and “obtained new state of the art results on … NLP tasks” (Devlin et al., 2019). In order to semantically

and contextually represent the abstract using BERT, it underwent some pre-processing. The given abstract was treated

as a single segment of data. After adding the classifier and separator tokens, the abstract was tokenized using

built-in tensorflow extensions for BERT. Tokenization involves converting all words into BERT tokens, and split up

any OOV (Out-of-Vocabulary) words into smaller tokens, prefixes, and suffixes. After tokenizing the data, it was

converted to indices to represent each token as an entry in BERT vocabulary, which is the reference index for BERT

to get the unique word embedding for the given vocabulary word.

Methods

Once the news articles were cleaned, abstracts extracted, and their content pre-processed into BERT indices, they

were fed to an evaluative BERT model to get context-driven document embeddings. The input here was the pre-set word

embeddings provided by BERT without the fine-tuning corresponding to the indices obtained through pre-processing.

For the proof-of-concept purposes, the initial classification token from the 12th hidden layer was used as a

representation of the abstract, and the abstract itself was treated as a single, order-independent sentence. Getting

document embeddings for headlines involved conversion of pre-processed data into tensorflow sensors to feed the

evaluative model.

The classification-level document embedding for each abstract is a 768-dimension vector, thereby mapping the given

abstract to context-based semantic space as shown below.

[Figure 1: A sample of abstract → vector mapping]

Here is a slice of our BERT vector document for a few of the news stories. In total, we have 69,404 of these vectors

where BERT has analyzed the language and mapped the data.

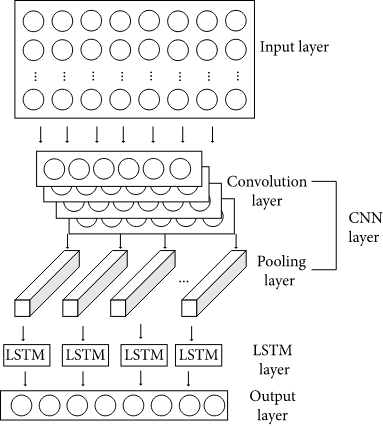

An LSTM network following the architecture shown below uses the context clues from document embedding of news

stories to predict the price increase or decrease due to the given news story. It is trained using the stock price

change as calculated from the data. This LSTM network uses neural networks to attempt to predict price increases. We

decided to use this model because recent research has shown that “the LSTM-based univariate model that uses one-week

prior data as input ... is the most accurate model.” (Mehtab et al., 2021)

[Figure 2: Architecture of LSTM memory cell]

Our LSTM model follows the basic structure with three hidden layers each having 10, 20, and 30 dense units. We used

non-linear activation function ReLu(rectified linear unit) as our activation function.

Then we set the look back period as a 60 days; therefore, the model predicts the future price based on the four

features of past 60 days. The followings are the four features we consider for each day. We selected close price and

volume from the raw data, and added new parameters $\text{high close ratio}$ and $\text{percent change}$ so that the

model could capture the overall tendency well.

$$ \begin{cases} \text{close price} & \\ \text{volume} & \\ \text{high close ratio} &= \frac{\text{high price} - \text{close price}}{\text{close price}} \\ \text{percent change} &= \frac{\text{close price} - \text{open price}}{\text{close price}} \end{cases} $$

_________________________________________________________________

Layer (type) Output Shape Param #

=================================================================

lstm (LSTM) (None, 60, 10) 600

_________________________________________________________________

dropout (Dropout) (None, 60, 10) 0

_________________________________________________________________

lstm_1 (LSTM) (None, 60, 20) 2480

_________________________________________________________________

dropout_1 (Dropout) (None, 60, 20) 0

_________________________________________________________________

lstm_2 (LSTM) (None, 30) 6120

_________________________________________________________________

dropout_2 (Dropout) (None, 30) 0

_________________________________________________________________

dense (Dense) (None, 1) 31

=================================================================

Total params: 9,231

Trainable params: 9,231

Non-trainable params: 0

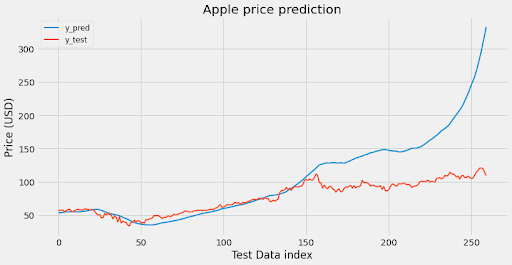

The 80 percent of the Apple stock data were used as the test data, and the model was trained by 10 epochs with batch size of 32. For the loss function, we used the mean squared error.

$$ MSE = \frac{1}{n} \sum_{i = 1}^{n}(Y_i - \hat{Y_i})^2 $$

_________________________________________________________________

Epoch 1/10

31/31 [==============================] - 13s 253ms/step - loss: 0.0773

Epoch 2/10

31/31 [==============================] - 8s 250ms/step - loss: 0.0200

Epoch 3/10

31/31 [==============================] - 8s 253ms/step - loss: 0.0141

Epoch 4/10

31/31 [==============================] - 8s 252ms/step - loss: 0.0102

Epoch 5/10

31/31 [==============================] - 8s 247ms/step - loss: 0.0083

Epoch 6/10

31/31 [==============================] - 8s 251ms/step - loss: 0.0085

Epoch 7/10

31/31 [==============================] - 8s 246ms/step - loss: 0.0078

Epoch 8/10

31/31 [==============================] - 8s 250ms/step - loss: 0.0074

Epoch 9/10

31/31 [==============================] - 8s 259ms/step - loss: 0.0066

Epoch 10/10

31/31 [==============================] - 8s 250ms/step - loss: 0.0066

Results and Discussion

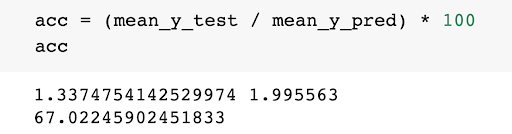

To summarize our results so far, we have collected news article data from the NYT developer API and stock price data from the yfinance library. We preprocessed the data by adding certain features like moving averages and daily change ratios to the Apple stock price. Then we analyzed the News Article data and organized the information into JSON files with information like abstracts, headlines, sources, and publication dates. After performing an analysis of the data, we reduced the number of dimensions by removing unnecessary features like the author, captions, url, and images to name a few. Then we created a LSTM model with neural networks for the Apple Price data using tensorflow and scikit that predicts Apple price data with an accuracy of 67%. For now we only have data on Apple but it’s very simple to query for other stock prices and rerun our model on the newly trained data. We also ran our BERT model on the New York Times articles and vectorized all 60,000 plus stories. Next our goal is to train the LSTM model on this data and see how much better the prediction becomes.

Analyzing this data found that the accuracy is about 67%. Next we’re planning on training our model with the BERT

tokens and seeing the new accuracy when we utilize context and sentiment in our program.

We will be adding the prices of Bitcoin (BTC) over time to our model as well, to better represent how a more

volatile entity (compared to AAPL) responds to the news cycle. This data will require a lot of cleaning, as BTC has

increased exponentially over time but we are looking to isolate the growth BTC has had due solely to general news.

Pooling is an important factor rather ignored in the present approach. One of the major ways to improve accuracy by

finding contextual relevance between news stories and stock prices is by generating more meaningful document

embeddings by experimenting with various types of pooling between output embeddings for abstracts to find an

approach that maximizes accuracy by accounting for outputs across words, layers, and sentence-based partitions

spanning across multiple model-based outputs. Similarly, once we do have a document embedding the target price can

drastically change based on the type of pooling used on all articles of the same day, determining the final price.

The approach to pool prediction by news story for all articles published in a day could significantly improve the

performance of the neural network. Another area of improvement is fine-tuning. When BERT is fine tuned to specialize

in news articles, it eliminates more noise, conveying more relevant information in the document embeddings

generated. Finally, predictions could increase through reinforcement learning, where the price change due to a given

news article is an input to a reward function, and the news articles in the past few days affect the stock price

change, instead of just the last business day. As a result, more complicated and long-term stories with evolving

timelines could be better represented in the stock price prediction, thereby improving the prediction accuracy

through greater comprehensivity.

References

- Devlin, J., Chang, M.-W., Lee, K., & Toutanova, K. (2019, May 24). BERT: Pre-training of Deep Bidirectional Transformers for Language Understanding. arXiv.org. https://arxiv.org/abs/1810.04805?source=post_page.

- Mehtab, S., Sen, J., & Dutta, A. (2021). Stock Price Prediction Using Machine Learning and LSTM-Based Deep Learning Models. Communications in Computer and Information Science, 88–106. https://doi.org/10.1007/978-981-16-0419-5_8

- Vanstone, B. J., Gepp, A., & Harris, G. (2019). Do news and sentiment play a role in stock price prediction? Applied Intelligence, 49(11), 3815–3820. https://doi.org/10.1007/s10489-019-01458-9